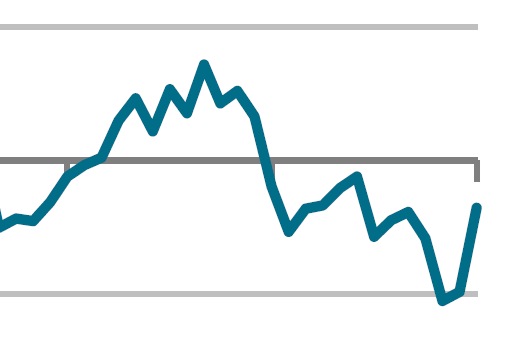

January knowledge indicated a miles slower decline in development output than on the finish of 2025.

At 46.4 in January, the seasonally adjusted S&P International UK Building Buying Managers’ Index (PMI) was once up sharply from December’s five-and-a-half yr low of 40.1.

All 3 sub-sectors recorded weaker charges of contraction than the ones noticed in December, helped by means of a extra solid call for atmosphere and experiences of a steady turnaround in gross sales pipelines.

Then again, inflation seems to be on the upward thrust once more, inhibiting development buying process.

The January PMI was once the absolute best since June 2025, however under the 50.0 no-change worth for the 13th month in a row, and indicating some other forged aid in general business process.

Space-building was once the weakest-performing section in January (index at 39.3), regardless that the tempo of contraction eased to its slowest for 3 months. Survey respondents cited a loss of new residential building tasks and subdued call for stipulations. Civil engineering process additionally lowered at a pointy tempo in January (40.6). However the most recent fall in business paintings (48.4) was once the slowest since Would possibly 2025. Some companies steered that post-budget readability and stepped forward investor sentiment had helped to stabilise call for within the business section.

Overall new paintings additionally lowered however to the least marked extent for 3 months. The place order books deteriorated, this was once ceaselessly attributed to chance aversion and fragile self belief amongst shoppers (particularly within the housing section). Then again, there have been some experiences of a turnaround in public sector paintings and gross sales enquiries for business tasks in the beginning of 2026.

Trade process expectancies for the yr forward persisted to rebound from the 35-month low noticed closing November. Round 38% of the survey panel are expecting a upward thrust in output volumes all through the following one year, whilst 17% foresee a discount. The ensuing index pointed to the absolute best stage of optimism since Would possibly 2025, despite the fact that self belief was once nonetheless smartly under the long-run survey moderate. Anecdotal proof cited decrease borrowing prices, larger infrastructure spending and hopes of a restoration in housing marketplace process as components more likely to give a boost to development workloads.

In the meantime, a strong and sped up building up in moderate price burdens introduced a problem for development corporations in January. The full fee of enter worth inflation was once the quickest since closing September. Survey respondents famous that providers had handed on upper uncooked subject matter and salary prices. Subcontractor fees additionally greater at a forged tempo, in spite of the sustained downturn in call for.

Squeezed margins and subdued order books weighed on development employment. Newest knowledge signalled some other aid in staffing numbers, extending the present length of process losses to 13 months.

In contrast background, buying process lowered sharply. January cutbacks most commonly mirrored a loss of new paintings to switch finished tasks.

Tim Moore, economics director at S&P International Marketplace Intelligence, which compiles the survey, mentioned: “January knowledge equipped encouraging indicators that the United Kingdom development sector has exited its tailspin, and companies are changing into extra hopeful that new tasks gets again on target in 2026.

“The newest aid in general business process was once the slowest since closing June. Industrial paintings outperformed, with process transferring on the subject of stabilisation amid a post-budget spice up to contract awards. Space constructing weak spot continued, despite the fact that even right here the speed of decline eased significantly since December and was once the least marked for 3 months.

“Building corporations famous subdued underlying call for because of fragile consumer self belief and increased chance aversion, however there have been some experiences of bettering funding sentiment and bigger gross sales enquiries in the beginning of the yr. Because of this, trade process expectancies rebounded to an eight-month top, whilst the tempo of process losses moderated.

“Provide stipulations stepped forward once more in January. Lead instances for the supply of development pieces shortened for the 6th month in a row and subcontractor availability greater at a forged tempo. Then again, margins have been beneath force as upper wages and uncooked subject matter costs resulted in the sharpest upward thrust in buying prices since September 2025.”

Brian Smith, head of price control at Aecom, mentioned: “A 2nd consecutive month of slowing decline means that the marketplace might be mountain climbing out of its stoop and contractors can see brighter days forward.

“We all know from our newest London Major Contractor Survey that self belief within the capital a minimum of will stay low for the momentary, however we’re seeing a wholesome stage of pageant available in the market and order books are nearing capability for 2026.

“What’s going to dictate when the marketplace makes a complete restoration is shoppers’ skill to transport ahead with tasks. Comfortable costs are emerging, as contractors cross on labour and subject matter prices, and sticky inflation implies that rates of interest aren’t being lower as temporarily as some can have was hoping.

“In the end, accelerating supply, discovering leading edge techniques to spice up competitiveness and diversifying tasks taken on are the hallmarks of a assured contractor this yr.”

Were given a tale? E mail information@theconstructionindex.co.united kingdom

{kind=link}