In keeping with the most recent S&P International Buying Managers’ Index (PMI), general building process ranges fell on the steepest tempo since Might 2020.

Underlying knowledge highlighted marked decreases in volumes of labor performed throughout all 3 monitored sub-sectors, however a substantial drag got here from a recent drop in residential constructing.

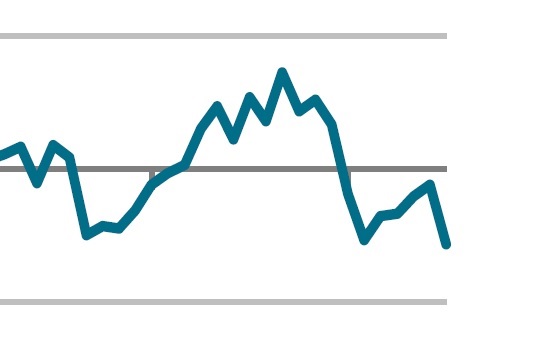

The headline PMI used to be 44.3 in July, down from 48.8 in June; the former post-covid low used to be a studying of 44.6 in February 2025. Any rating under 50 signifies a decline in process. The decrease the rating, the steeper the decline.

July’s rating used to be perilously as regards to June 2019’s studying of 43.1, which – the pandemic apart – stays a 15-year low.

Respondents blamed web site delays, decrease volumes of incoming new industry and weaker buyer self belief for July’s deficient appearing.

Some respondents additionally cited a discount in public sector paintings, with civil engineering seeing the sharpest drop throughout July. There used to be a renewed decline in residential constructing process whilst industrial building declined extra gently.

The amount of recent incoming paintings declined for a 7th month operating in July, in line with this survey, with the tempo of contraction at its maximum pronounced since February. A drop in comfortable alternatives used to be cited.

Having a look forward to the following three hundred and sixty five days, surveyed firms have been constructive of enlargement in process, on stability, however expectancies have been susceptible when put next with their long-run development. This used to be regardless of industry self belief ticking up moderately from June’s two-and-a-half-year low. Considerations surrounding the wider financial outlook weighed on corporate enlargement projections.

The downward development in payroll numbers endured into July, extending the present length of falling employment to seven months. Lay-offs, recruitment freezes and the non-replacement of leavers have been observed in panellists’ anecdotal replies to the questionnaire.

UK constructors additionally pared again their utilization of subcontractors, however their charges charged nonetheless rose at a pointy tempo, in step with the fashion observed since past due ultimate 12 months.

Joe Hayes, primary economist at S&P International Marketplace Intelligence, stated: “Having trended upwards in fresh months, our survey knowledge for July sign a recent setback for the United Kingdom building sector, with general trade process falling on the sharpest price since Might 2020. Dissecting the most recent contraction, we will see a recent and sharp drop in residential constructing, in addition to an sped up fall in paintings performed on civil engineering tasks.

“Ahead-looking signs from the survey indicate that UK constructors are making ready for difficult occasions forward. They are purchasing much less fabrics and decreasing the choice of staff at the payroll. Expectancies additionally proceed to underwhelm, regardless of a modest pick-up in self belief from June’s two-and-a-half-year low.

“Anecdotally, firms reported a loss of comfortable alternatives and a hesitancy from consumers to decide to tasks. Broader topics of uncertainty, each locally but in addition across the world, will do little to reignite funding appetites.”

Gareth Belsham, director of Bloom Development Consultancy, commented: “There’s no sugarcoating it – this knowledge will probably be tricky to swallow for just about everybody in building.

“All 3 subsectors of the trade noticed output contract in July, with the sharpest fall coming in civil engineering. Area-building, the sphere cherished of politicians short of a photograph opp, additionally declined badly.

“To make issues worse, the pipeline of recent paintings is drying up rapid. New order numbers have now fallen for seven months in a row, with July’s hunch the worst observed since February. Little marvel contractor self belief is susceptible and plenty of building corporations are shedding payrolled personnel.

“June noticed sentiment plunge to its lowest degree since December 2022, and whilst July’s determine advanced marginally, even essentially the most constructive of developers will to find it onerous to peer the glass as half of complete.

“The next day the Financial institution of England is broadly anticipated to chop its base price for the 3rd time this 12 months, and the chance of inexpensive finance will probably be welcomed through builders who’re suffering to sq. their finance prices with susceptible call for for his or her finish product.

“The only shiny spot is industrial sector building. Whilst it too noticed output fall in July, no less than extra industrial schemes are being greenlit. Those who do are laser-focused on price and feature an absolutely costed industry case – there may be minimum margin for error.”

Were given a tale? E mail information@theconstructionindex.co.united kingdom

{kind=link}