After 10 consecutive months of emerging output, January noticed UK building fall again.

Shrinking order books and emerging value pressures contributed to the weakest trade task expectancies since October 2023, in keeping with buying managers.

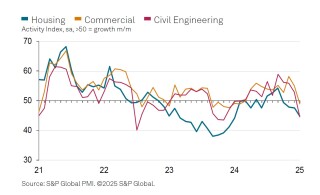

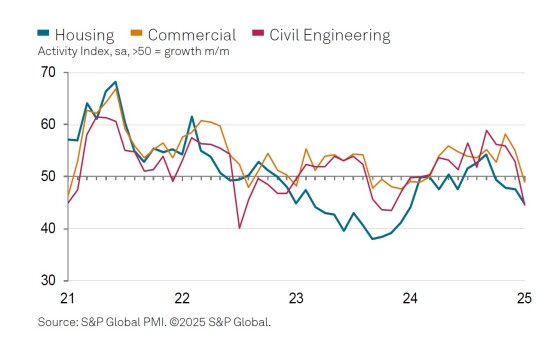

At 48.1 in January, down considerably from 53.3 in December, the headline seasonally adjusted S&P World UK Building Buying Managers’ Index (PMI) registered under the 50.0 no-change threshold for the primary time since February 2024. (The rest above 50.0 point out expansion; under signifies dwindling output.)

Building firms cited behind schedule decision-making via shoppers on main tasks and normal financial uncertainty had weighed on trade task at first of 2025. Numerous corporations additionally commented at the affect of subdued marketplace prerequisites within the residential constructing sector.

All 3 huge sectors of the business moved into detrimental territory in January. Area-building (index at 44.9) diminished for the fourth successive month and on the quickest tempo since January 2024. Civil engineering task (44.6) declined at a somewhat sharp charge, even supposing this partially mirrored disruptions from surprisingly rainy climate at first of the yr. Industrial building class additionally returned to contraction in January (48.9). This used to be related to a loss of smooth alternatives and a reluctance amongst shoppers to decide to new tasks.

January information pointed to a decline in incoming new paintings for the primary time in one year. Even if simplest modest, the velocity of contraction used to be the steepest since November 2023. Anecdotal proof urged {that a} insecurity amongst shoppers and worries about the United Kingdom financial outlook had contributed to fewer gross sales enquiries.

Buying task diminished for the second one month in a row, reflecting vulnerable order books and a loss of new paintings to exchange finished tasks. Regardless of softer call for for building merchandise and fabrics, the newest survey indicated the steepest upward push in enter prices since April 2023. Building firms famous that providers had sought to go on emerging power, transportation and personnel prices. Additionally, dealer efficiency deteriorated to the best extent for 2 years, which used to be partially related to delivery delays.

Tim Moore, economics director at S&P World Marketplace Intelligence, which complies the per month survey, stated: “UK building output fell for the primary time in just about a yr as gloomy financial possibilities, increased borrowing prices and vulnerable consumer self belief led to subdued workloads.

“Output ranges diminished around the board in January, with in particular sharp discounts noticed within the residential and civil engineering classes.

“Building corporations famous the quickest fall in residential paintings for one year as marketplace prerequisites remained moderately subdued. Anecdotal proof urged that warning relating to call for for brand spanking new tasks used to be prevalent at first of 2025, regardless of robust coverage give a boost to for house-building and hopes for a longer-term spice up to provide by way of making plans reform.

“The forward-looking survey signs had been additionally somewhat downbeat in January. New orders diminished on the quickest tempo since November 2023 amid many experiences of behind schedule decision-making via shoppers. Decreased workloads, mixed with considerations in regards to the normal UK financial outlook, resulted in a dip in trade task expectancies to the bottom for 15 months.

“There used to be little respite at the provide entrance, as delivery delays supposed that dealer lead instances lengthened to the best extent for 2 years. Call for for building pieces softened once more in January, however acquire value inflation used to be the best since April 2023 as providers sought to go on emerging power, gasoline and salary prices.”

Brian Smith, head of value control and industrial at Aecom, commented: “A iciness slowdown is unsurprising given the wider financial temper however self belief will want to beef up temporarily if the field is to regain a few of 2024’s momentum and ship at the govt’s expansion time table.

“After a sobering begin to 2025, corporations shall be hoping to look additional cuts to rates of interest that inspire shoppers to green-light tasks and unharness extra non-public funding during the yr.

“That stated, contractors’ expansion possibilities are just right this yr, with pipelines suggesting there may be enough paintings to head round. The rate of supply although may well be challenged their willingness to tackle important quantities of recent paintings given the volatility of new years and long-standing demanding situations round labour availability.”

Terry Woodley, managing director of construction finance at cash lender Shawbrook, stated: “The opposed climate put a undeniable dampener on task this month, with building output dipping, in addition to the ongoing declines in spaces corresponding to civil engineering. Now not all has been misplaced, on the other hand, as builders have replied undoubtedly to the Chancellor’s contemporary speech on expansion through which she defined the following steps in streamlining making plans selections to make sure the 1.5 million new houses goal is met.

“Despite the fact that a welcome replace, there are nonetheless considerations across the present abilities scarcity within the sector, which might stand in the best way of Labour’s imaginative and prescient of ‘shovels within the flooring and cranes within the sky’. Building task has the prospective to take off this yr, however till those problems are addressed, the field dangers being held again.”

Atul Kariya, head of actual property and building at accountancy crew MHA, stated: “It’s infrequently unexpected that building PMI task has fallen because the business and the financial system as an entire at the moment are beginning to see the entire affect of the proposed tax rises and greater labour prices within the autumn finances. Those are beginning to feed thru into total trade sentiment within the sector in addition to ongoing difficult financial prerequisites in the United Kingdom and out of the country. The glimmers of optimism that the business witnessed in September final yr when the PMI soared to 57.2 now appear a bit of far-off, regardless of order ebook and enquiry ranges closing somewhat buoyant.

“Despite the fact that there was a contemporary an building up in dwelling gross sales that is in all probability to had been pushed via the approaching building up in stamp responsibility in April which is mirrored in proportion values around the sector as housebuilders are recently buying and selling even less than they did all the way through the pandemic.

“The housebuilding sector has witnessed a pointy decline regardless of the federal government’s making plans reforms on housing which might be because of be kickstarted within the spring, whilst industrial building additionally noticed a decline in output as anxiety stays round the United Kingdom’s financial expansion.

“Whilst the fast time period outlook stays gloomy we’re hopeful that with successive cuts in rates of interest during 2025, expected to start out as of late, there shall be a pickup in task and optimism within the sector.”

Were given a tale? Electronic mail information@theconstructionindex.co.united kingdom

{kind=link}