December 2024 noticed general development task increasing on the slowest tempo since closing June, whilst new order expansion moderated for the 3rd month operating.

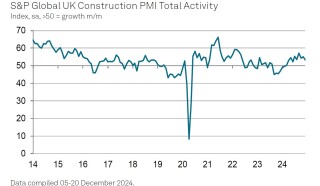

The headline S&P International UK Development Buying Managers’ Index (PMI) registered 53.3 in December, down from 55.2 in November and the bottom for 6 months. That stated, the index has posed above the a very powerful 50.0 no-change worth since March 2024.

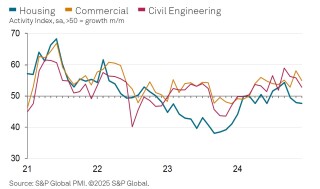

Industrial task used to be the fastest-growing house of the development sector in December (index at 55.0), adopted by way of civil engineering (52.9), even though each rankings have been down on November. The survey is seasonally adjusted, so the truth that December noticed many websites close down for the festive duration isn’t an element.

Residential paintings used to be once more the one class to check in an general decline in output throughout December (47.6). Area-building task has now diminished for 3 consecutive months and the most recent aid used to be the quickest since June 2024. Survey respondents famous that subdued call for, increased borrowing prices and vulnerable client self belief had all weighed on task.

Mirroring the craze for output volumes, general new paintings additionally expanded on the slowest price since closing June. Anecdotal proof instructed that making improvements to delicate alternatives within the business constructing sector have been offset by way of cutbacks to residential construction initiatives and a loss of new industry to switch finished infrastructure paintings.

Development firms spoke back to weaker new order expansion by way of lowering their enter purchasing for the primary time in 8 months, the survey discovered. In some cases, decrease ranges of buying task have been related to tighter stock control. Providers’ supply instances have been widely unchanged in December. Whilst some companies famous making improvements to dealer efficiency because of decrease call for, there have been additionally experiences that transport delays had resulted in longer lead instances for imported pieces.

December information highlighted a decline in subcontractor utilization for the fourth time previously 5 months. In spite of decrease call for for his or her services and products, subcontractor availability advanced most effective marginally and on the slowest tempo since March 2023.

In the meantime, newest information indicated the quickest upward push in charges charged by way of subcontractors for 20 months. Including to upward power on enter prices, acquire costs greater at a tempo that used to be most effective relatively softer than November’s 18-month excessive. Increased value inflation and emerging wage bills have been once more cited as components maintaining again personnel hiring. The tempo of process advent remained less than the pre-pandemic reasonable.

Having a look forward, round 48% of the survey panel are expecting a upward push in output over the process 2025, whilst most effective 15% forecast a decline. The level of sure sentiment picked up sharply since November, nevertheless it used to be nonetheless a lot weaker than noticed within the first half of of 2024. Whilst development companies normally commented on optimism related to long-term industry enlargement plans, many additionally cited worries concerning the basic UK financial outlook and tighter budgets for capital spending.

Tim Moore, economics director at S&P International Marketplace Intelligence, which conducts the per thirty days survey, stated: “December information highlighted a lack of momentum for development output expansion, with all 3 primary classes of task posting weaker performances than within the earlier month. Industrial constructing maintained its place because the fastest-growing house of development task, adopted by way of civil engineering. Against this, residential paintings diminished for the 3rd month operating and on the quickest tempo since June 2024.

“The slowdown in general development output expansion mirrored extra subdued call for stipulations in fresh months, as illustrated by way of an extra moderation in new order expansion throughout December. Survey respondents commented on headwinds from increased borrowing prices and the affect of fragile client self belief.

“Team of workers hiring picked up since November, however there have been indicators of tight provide stipulations. Sub-contractor availability advanced to the smallest extent since March 2023, whilst the charges they charged greater on the quickest tempo for simply over one-and-a-half years.

“Issues concerning the call for outlook weighed on development sector expansion expectancies for 2025. Even if self belief recovered after a post-budget stoop throughout November, it used to be nonetheless a lot weaker than within the first half of of 2024. Many companies reported worries about cutbacks to capital spending and gloomy projections for the United Kingdom economic system.”

Brendan Sharkey, actual property and development specialist at accountancy workforce MHA, stated: “The autumn in development PMI is infrequently sudden because the trade continues to get pleasure from the federal government’s funding in infrastructure however on the identical time is hampered by way of nonetheless traditionally excessive rates of interest and an uptick in employment prices.

“Process within the business sector stays robust, however housing has dipped. Whether or not the housing marketplace will see a reversal in fortunes this yr is still noticed, then again the chance to increase is obviously there given the making plans reforms integrated within the fresh NPPF (Nationwide Making plans Coverage Framework). Total, the development trade has been slightly resilient in 2024 in comparison to different business sectors. Call for for development could be very a lot on a home degree, while production and different business sectors are reliant at the international economic system.

“From what our purchasers are telling us, 2025 is anticipated to be higher than closing yr; then again, it’ll be a gradual burn. Infrastructure will do neatly given the federal government’s funding plans as will business as the United Kingdom is changing into an funding selection for lots of. Housing provide will probably be to be had nevertheless it’s whether or not call for will practice if rates of interest stay stubbornly excessive.

“Whilst excessive rates of interest and lengthening labour prices will proceed to have an affect at the trade, an greater waft of inward funding will have to supply some aid.

“We think that development PMI will hover round the similar degree as it’s these days for a lot of 2025, and any spikes usually are short-lived. Even if expansion will probably be gradual and secure the basics for the sphere are forged and there may be an air of quiet optimism.”

Were given a tale? E-mail information@theconstructionindex.co.united kingdom

{kind=link}